According to the latest data from Auto Trader’s Retail Price Index, which is based on pricing analysis of circa 900,000 vehicles every month, August saw the largest monthly price increase ever recorded on its marketplace.

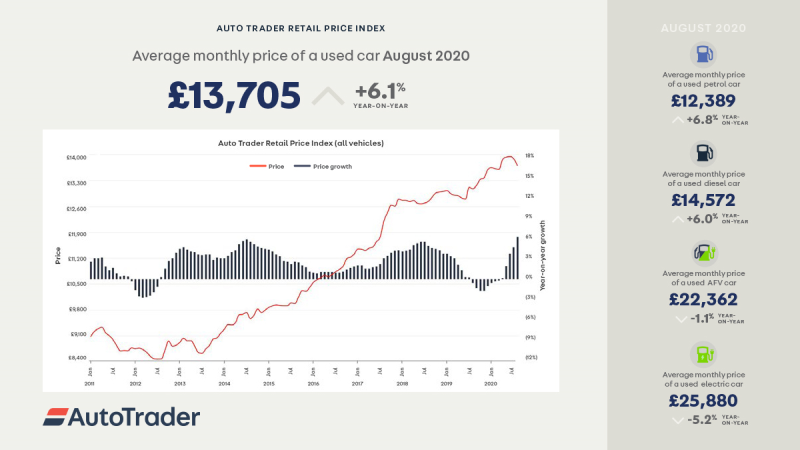

The average retail price of a used car last month was £13,705, which marks a 6.1% year-on-year (YoY) increase on a like-for-like basis and five months of consecutive growth.

Go deeper with GlobalData

It’s also the steepest month-on-month increase in the rate of growth, leaping from 4.6% in July.

Average prices in August were affected by several different factors, including the mix of stock within the market.

Last month there were fewer diesels, automatics and cars aged under one-year-old in the market, which as a result meant price growth was slowed down by a decline in these more expensive segments.

Whilst supply challenges remain for many retailers, demand continues to grow at record levels.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataOn Auto Trader, the huge traffic in June (64m) and July (64.4m) has accelerated dramatically in August, with a staggering 67.1m cross-platform visits to its marketplace: a year-on-year increase of 30.5%.

Taking a more granular view of the market, due in part to demand outpacing supply, internal combustion engine (ICE) vehicles continued to record strong rates of price growth in August.

Taking a more granular view of the market, due in part to demand outpacing supply, internal combustion engine (ICE) vehicles continued to record strong rates of price growth in August.

As highlighted on Auto Trader’s Market Insight analytics tool, available to all retailers, demand for petrol cars increased 27.4% YoY last month, whilst supply was down -3.6%.

As a result, the average sticker price for a used petrol car increased 6.8% (£12,389) in August, the ninth month of consecutive growth.

Diesel recorded a similarly positive performance. However, whilst demand was up 19.3% YoY, supply of second-hand diesels in the market fell a significant -20.3% in August.

It contributed to a 6% YoY (£14,572) price increase, the highest ever rate of growth for second-hand diesel cars recorded on the Retail Price Index (RPI).

In contrast to their ICE counterparts, since the beginning of the lockdown period demand for low-emission vehicles has fallen below levels of supply.

It suggests car buyers are reverting to the type of vehicles they are familiar with, and what they consider to be the most affordable choice, namely petrol and diesel cars.

In August, the average price of an EV was £25,880, a -5.2% decline on the same period last year, and the highest rate of contraction since November 2015.

Alternatively fuelled vehicles (AFV) more broadly fared slightly better, with average prices declining -1.1% (£22,362); the sixth consecutive month of price contraction.

In terms of body types, whilst hatchbacks saw the highest average price increase (10.7%) last month, SUVs continue to record the highest level of demand at 37% YoY. However, they recorded the lowest rate of price increases at 2.9%, which is due in part to the high level of supply. Last month, SUVs represented 27% (87,348) of total supply into the market.

In August every age band of used car recorded an average price increase. Vehicles aged 10-15 years saw the highest rate of growth, surging 13.4% (£4,281). In contrast, vehicles aged one to three years old saw the lowest rate of growth at 3.9% (£18,684).

Both premium and volume brands saw average prices grow in August, increasing 3.9% (£20,710) and 11.5% (£9,065) respectively. While demand outstripped supply in both segments, premium brands continue to show stronger performance compared to volume brands, increasing 27% versus 23%.

Richard Walker (pictured above), director of data and insight for Auto Trader, said: “Over the last five months we’ve observed a very positive trajectory for used car prices, driven largely by supply challenges and extremely strong consumer-led demand.

“Although some of the supply constraints had begun to ease with the reopening of online auctions, many of our customers are reporting that they continue to face difficulty in sourcing wholesale stock. Combined with the massive acceleration in demand on our marketplace, whilst the trajectory may begin to level off slightly, we’re confident prices will remain buoyant over the coming months.

“It’s very reassuring to see such huge demand in the market as we enter into what will be a key month for the industry on its road to recovery. September is typically the second-highest monthly volume for new car, but as March was cut short and with such exceptionally strong consumer metrics, it may very well represent the largest sales month of 2020.”

During the lockdown, the number of retailers making price changes and the value of price adjustments was significantly lower than normal trading conditions. This has increased following the reopening of showrooms in June; however, it remains below pre-COVID-19 levels.

In August, the average number of retailers making daily price changes was 1,982; 17% fewer than in August 2019. The average amount being changed daily was £263, which was a 28% decline on the same time last year.

Sue Robinson, director of the National Franchised Dealers Association (NFDA), said: “Used car prices are benefitting from strong consumer demand alongside supply challenges. Demand for internal combustion engine cars continues to be buoyant in the used sector, which is reflected in the average price increase for petrol and diesel vehicles.

“We expect appetite for used cars to remain robust over the coming weeks thanks to a number of factors including the movement away from public transport to owned vehicles and the increase in disposable income for a number of consumers”.